Published February 1, 2026

Buying a Home Is Finally Getting More Affordable (Yes, Really)

After a long stretch of discouraging headlines, there’s finally some good news for buyers who’ve been priced out or stuck waiting on the sidelines: buying a home is becoming more affordable.

Monthly payments are starting to ease, and while that doesn’t mean the market is suddenly “easy,” the pressure buyers have felt over the past few years is slowly loosening. In a market that’s felt relentless, even gradual improvement is worth paying attention to.

Affordability Is Moving in the Right Direction

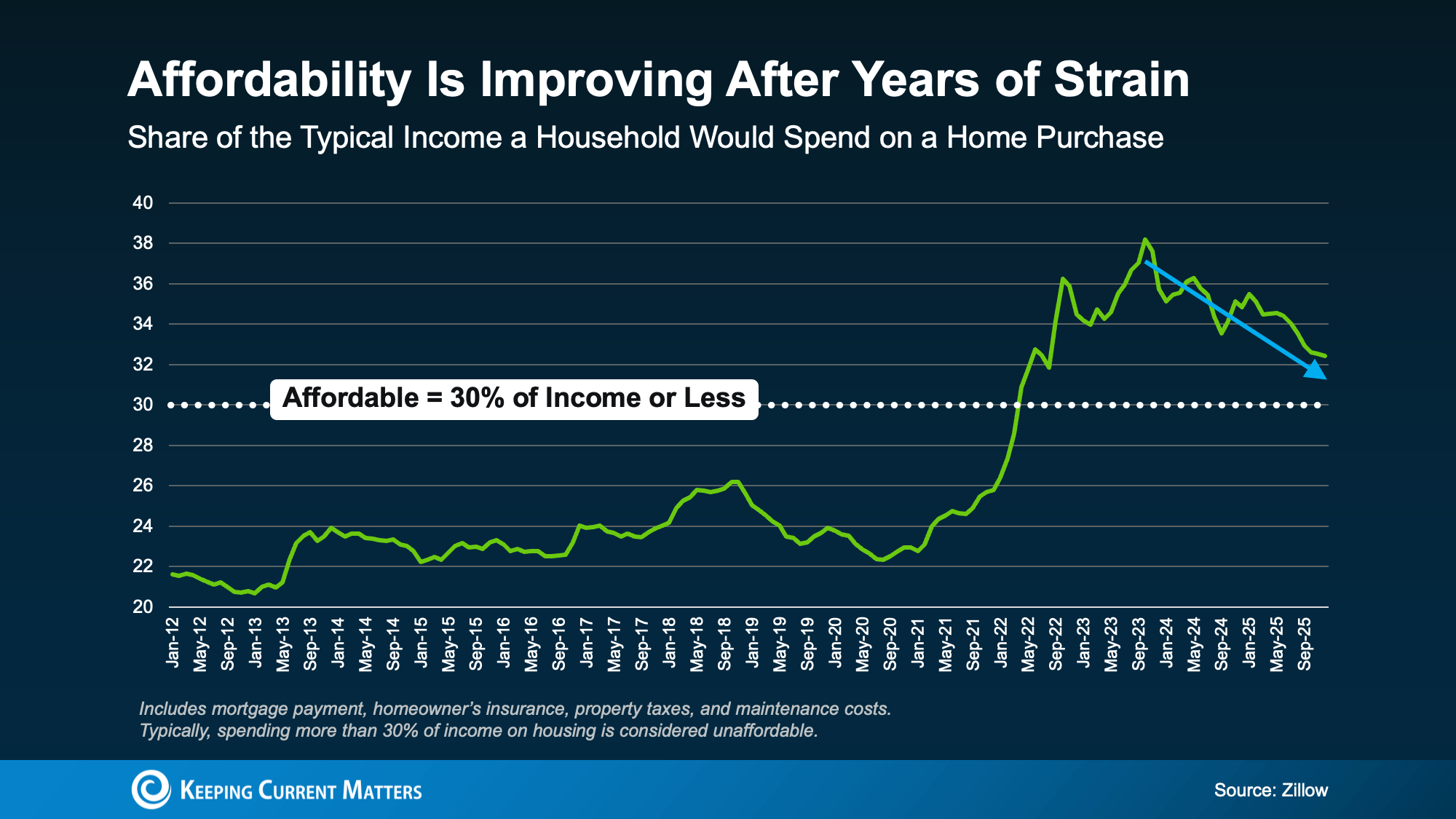

One of the clearest ways to see this shift is by looking at how much of a household’s income goes toward owning a home.

Zillow considers housing affordable when total housing costs — including mortgage payments, taxes, insurance, and basic maintenance — take up 30% or less of monthly income. For several years, buyers were well above that benchmark, making homeownership feel out of reach for many.

Now, that math is improving. Zillow data shows that it’s taking less of a typical household’s income to buy a home than it did just a few years ago.

We’re not fully back to that 30% affordability threshold yet, so conditions are still tight. But the direction matters — and right now, things are trending the right way.

Why Affordability Is Improving

Mortgage rates get most of the attention, and yes, they’re playing a role. But they’re not the only factor helping buyers right now. Three key trends are working together to improve affordability:

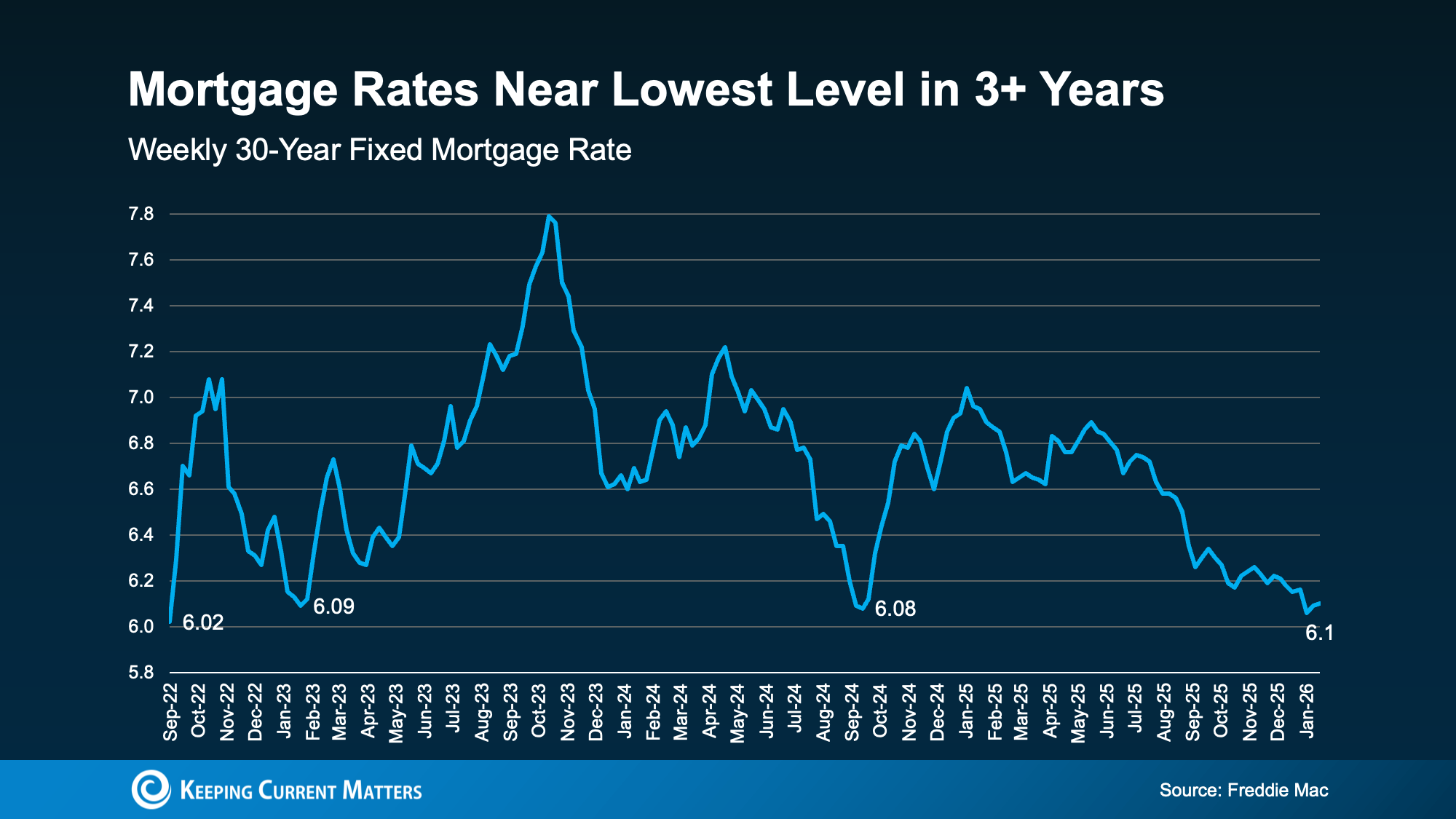

1. Mortgage rates have eased.

Rates are hovering near their lowest levels in more than three years, which directly lowers monthly payments for buyers.

2. Home price growth has cooled.

Prices aren’t falling nationally, but they’re no longer rising at the breakneck pace we saw a few years ago. Slower growth means buyers aren’t chasing rapidly increasing prices, making monthly payments more predictable and manageable.

3. Wages are growing faster than home prices.

This is a big one. As Mark Fleming, Chief Economist at First American, explains:

“When income growth exceeds house price growth, house-buying power improves — even if mortgage rates don’t decline meaningfully.”

None of this makes buying inexpensive, but it does explain why the numbers are finally starting to work a little better than they did even a year ago. The same forces that crushed affordability are now easing. Fleming puts it this way:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

Because of these combined trends, economists expect affordability to continue improving through 2026.

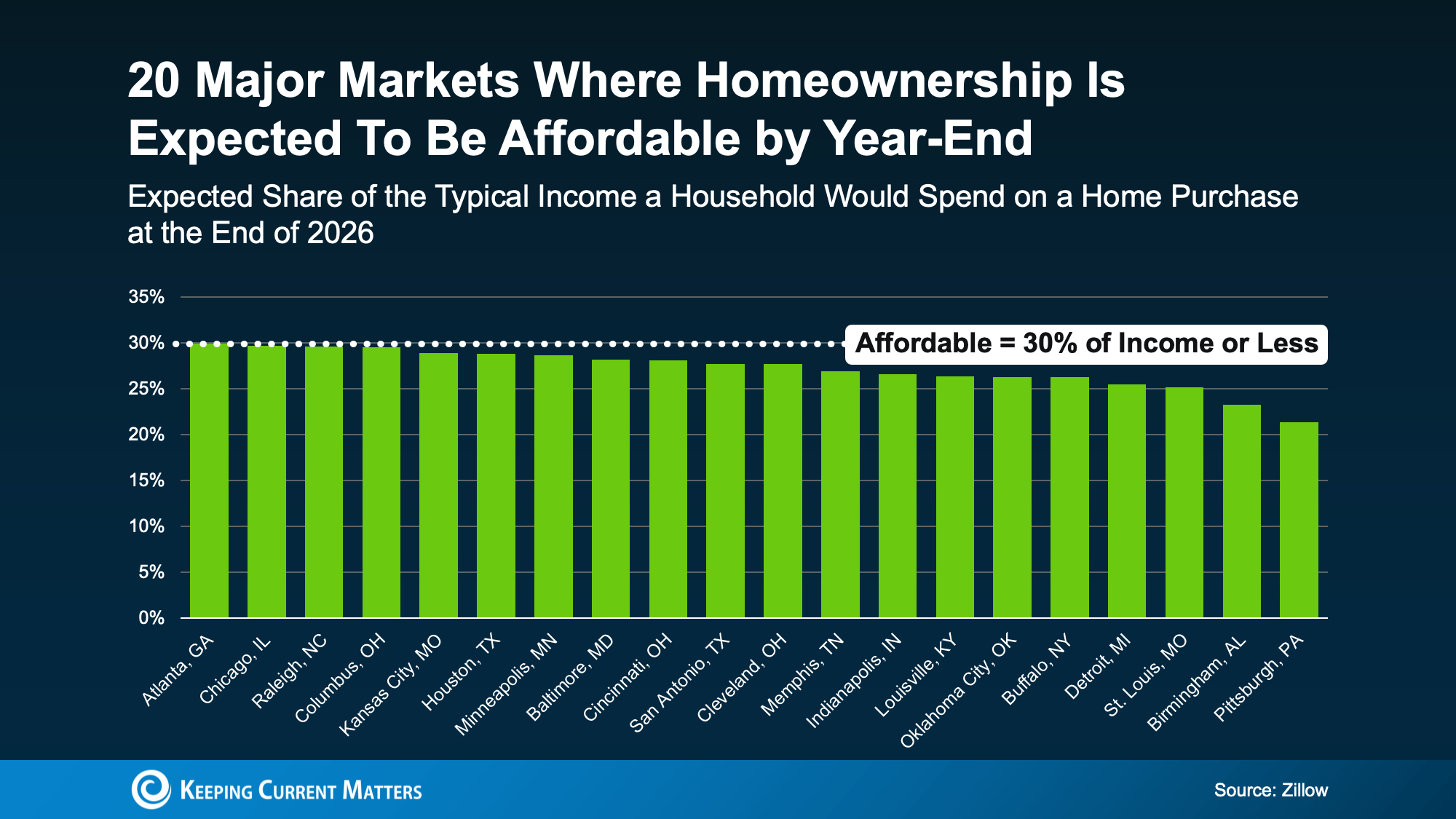

Where Affordability Is Improving First

So what does this mean in real life? In some markets, the impact will be noticeable sooner than others. Zillow projects that certain areas could fall back under the 30% affordability threshold by the end of the year.

That doesn’t mean you need to live in one of those markets — or wait until year-end — to make a move. Many areas are already seeing meaningful improvements. The key is understanding how national trends show up locally.

Bottom Line

For the first time in quite a while, housing affordability is easing, and that’s a meaningful shift for buyers.

Because this change isn’t happening at the same speed everywhere, local insight makes all the difference. If you want to understand what these trends look like in your market — and whether buying now makes sense for you — Rucker and Associates is the team to reach out to for guidance grounded in real, local data.