Published April 1, 2026

Focus on What You Can Control in Today’s Mortgage Market

Mortgage rates have been anything but steady lately—and if you’re thinking about buying, that can make planning feel a little uncertain. The good news? Even in a shifting market, there are still ways to put yourself in the best possible position. It all starts with understanding what’s actually happening and where you have control.

Why Are Mortgage Rates Moving?

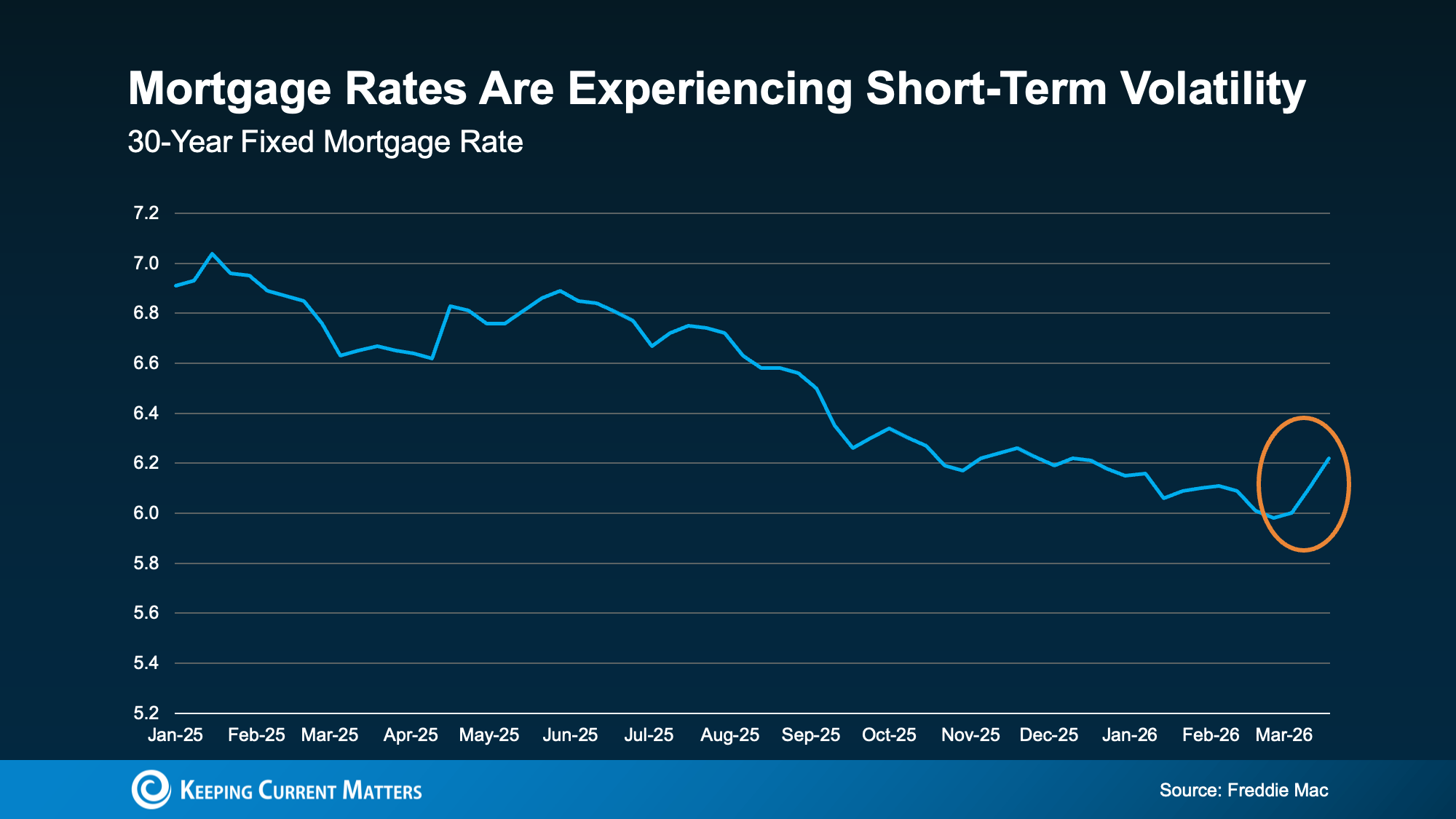

If you’ve been watching the headlines, you’ve probably noticed rates have been bouncing around. After trending downward for quite some time, they’ve ticked back up recently.

While that kind of movement can feel discouraging, it’s important to zoom out. Small ups and downs like this are completely normal. Even over the past year, we’ve seen similar moments where rates briefly climbed before leveling out again.

A big reason for this? The broader economy. Mortgage rates are influenced by inflation, the bond market, and even global events. When there’s uncertainty—whether economic or geopolitical—rates tend to react quickly. That’s just the nature of the market.

And that’s exactly why trying to “time” your purchase around rates isn’t always the best strategy. The reality is, no one can predict where they’ll go next with certainty.

What You Can Control

Even though you can’t control the market, you’re not powerless. There are a few key factors that directly impact the rate you’ll qualify for—and this is where your focus should be.

Your Credit Score

Your credit score is one of the biggest drivers of your mortgage rate. The stronger your score, the better your chances of securing a lower rate and more favorable terms. Even a small improvement can have a noticeable impact on your monthly payment.

If you’re unsure where you stand, this is a great place to start. A quick conversation with a lender can help you understand your score—and what steps, if any, could help improve it.

Your Loan Type

Not all loans are created equal. From conventional to FHA, VA, and USDA loans, each option comes with different requirements, benefits, and rate structures.

Exploring your options matters more than most buyers realize. The right loan for your situation could make a meaningful difference in both your upfront costs and your long-term payment. This is where working with a knowledgeable lender really pays off.

Your Loan Term

The length of your loan also plays a role in your rate. Whether you’re considering a 15-, 20-, or 30-year mortgage, each option comes with its own balance of monthly payment, interest rate, and total cost over time.

A shorter term often means a lower rate but higher monthly payments, while a longer term can offer more flexibility month-to-month. The right fit depends on your goals, your budget, and how long you plan to stay in the home.

The Bottom Line

Mortgage rates will always have some level of unpredictability—that’s not something you can control. What you can control is how prepared you are when you step into the market.

Focusing on your credit, exploring the right loan options, and understanding your numbers puts you in a much stronger position—no matter what rates are doing.

If you’re thinking about making a move, reach out to your Rucker and Associates agent and a trusted lender to talk through your options and build a plan that works for you.