Published May 1, 2025

Mortgage Rates Won’t Sit Still—Here’s What You Can Do

What’s Going On with Mortgage Rates? And What Can You Actually Do About It?

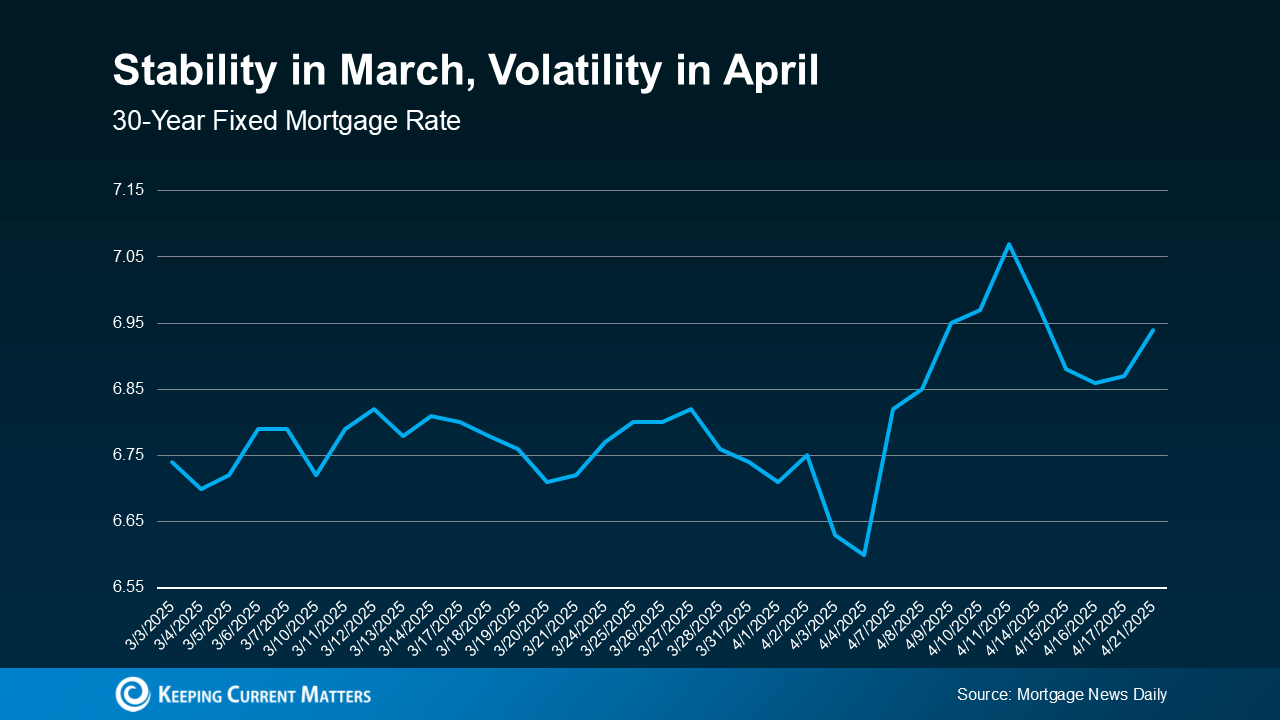

Have you noticed how unpredictable mortgage rates have been lately? One day they dip, and the next they bounce right back up. If you’re thinking about buying a home, that kind of volatility can be frustrating—and downright confusing.

As you can see, rates stayed relatively steady through March, but April has been more of a roller coaster ride. This kind of up-and-down movement is typical when the economy is shifting. And while it’s totally normal to wonder if now is the right time to buy, trying to time the market perfectly is nearly impossible.

Here’s the good news: you don’t have to sit back and hope for the best. While you can’t control mortgage rates, there are things you can control that will help you lock in the best possible rate for your situation.

1. Your Credit Score

Your credit score plays a major role in what kind of rate you’ll qualify for. Even a small increase in your score could mean a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

Not sure where your score stands or how to improve it? A trusted loan officer can help you make a game plan.

2. Your Loan Type

Not all loans are created equal. The type of loan you choose—conventional, FHA, USDA, or VA—can impact your eligibility and your interest rate.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans... Rates can be significantly different depending on what loan type you choose.”

That’s why it’s a smart move to talk to multiple lenders and figure out what loan best fits your needs.

3. Your Loan Term

Loan terms—how long you take to repay your mortgage—also affect your rate and monthly payment. Most buyers choose 15, 20, or 30-year terms.

According to Freddie Mac:

“Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Be sure to ask your lender to walk you through your options.

Bottom Line

Mortgage rates are constantly moving, and trying to predict what they’ll do next isn’t easy. But you don’t have to just wait and see. By taking control of your credit, loan type, and loan term, you can put yourself in a strong position to buy—whenever the time is right for you.

Have questions? Let’s connect. The Rucker and Associates Team would be happy to put you in touch with a trusted lender and talk through your next steps.